Mortgage Rates Since 2000

A Data-Driven Journey Through Economic and Policy Cycles

Robert G Premecz, SRA

7/1/20253 min read

Mortgage Rates Since 2000: A Data-Driven Journey Through Economic and Policy Cycles

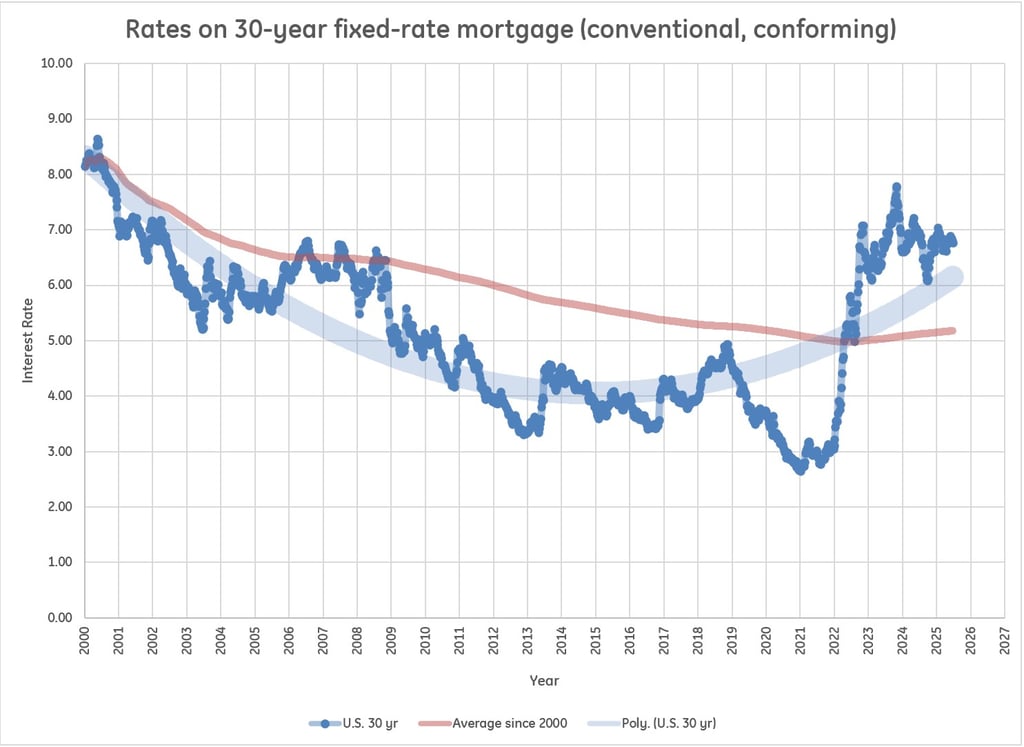

As a real estate appraiser, I track mortgage rates not just out of curiosity—but because they influence buyer behavior, affordability, market velocity, and, ultimately, home values. The chart above illustrates how 30-year fixed mortgage rates have shifted from 2000 through 2025. And behind every rate movement is a mix of monetary policy, fiscal stimulus, global events, and consumer psychology.

Here’s a professional, yet plainspoken look at what happened—and why it matters.

2000–2008: A Period of Gradual Decline, Then Collapse

The early 2000s began with rates in the 7–8% range. They steadily declined due to a combination of post-dot-com recession recovery and Fed easing following the events of 9/11. Mortgage availability expanded. Underwriting standards weakened. Homeownership surged—but so did systemic risk.

Key event: The 2008 housing crisis, fueled by risky lending, over-leveraged financial institutions, and inflated valuations.

Appraisal impact: Pressure on appraisers increased during the boom; after the crash, regulatory oversight tightened dramatically (HVCC, then Dodd-Frank).

2009–2016: Post-Crisis Stability and Ultra-Low Rates

Under the Obama administration, the Fed adopted Quantitative Easing (QE), purchasing mortgage-backed securities to lower borrowing costs. Rates remained in the 3.5–4.5% range, reaching new historical lows.

Market effect: Buyers re-entered cautiously; refinance activity exploded.

Appraisal considerations: Market value definitions held firm, but appraisers often had to explain the lag between market recovery and consumer confidence.

2017–2020: Volatility and the COVID Response

Rates began rising slightly under the Trump administration due to tax policy and economic expansion. Then, in 2020, the COVID-19 pandemic prompted a swift monetary response. The Fed dropped its benchmark rate, triggering mortgage rates to fall below 3%—a once-in-a-generation phenomenon.

Buyer behavior: Record-low rates caused a dramatic surge in demand and price appreciation.

Appraiser insight: Rapid appreciation, multiple offers, and waived contingencies presented valuation challenges, particularly when comps lagged.

2021–2024: Inflation, Intervention, and Rate Shock

The post-pandemic economy saw stimulus-fueled demand, supply chain constraints, and ultimately, high inflation. The Federal Reserve responded with aggressive rate hikes, pushing mortgage rates from the low 3s to above 7% within two years.

Context: Both parties contributed—fiscal stimulus under Trump 1.0 (COVID-era) and Biden’s recovery policies increased liquidity.

Appraisal shift: The sharp rise in rates cooled buyer enthusiasm, caused price flattening in some markets, and increased time on market.

2025: Plateauing, Not Plummeting

So far, 2025 has seen rates hover in the 6.5–7.5% range. While many expected relief by mid-year, the Fed has remained cautious. Sticky inflation, wage growth, and geopolitical uncertainty have made policymakers hesitant to cut too soon.

Consumer perception: Many buyers remain anchored to ultra-low pandemic rates and view today’s rates as “high,” even though they remain near the 50-year average.

Appraiser note: Affordability constraints may continue to limit appreciation in many markets, particularly for first-time buyers.

Historical Context and Political Framing

From an appraisal standpoint, it's important to remain politically neutral—economic trends transcend party lines:

Republican policies have generally emphasized deregulation and tax incentives, which can stimulate construction and ownership but also risk overheating markets if unchecked.

Democratic policies often emphasize housing access, financial oversight, and stimulus in downturns, which can improve equity but risk inflationary pressure.

Neither party owns the mortgage rate story. Instead, it’s shaped by global markets, inflation expectations, Federal Reserve decisions, and consumer sentiment. Presidents don’t set mortgage rates, but their actions and appointees (especially to the Fed) influence the environment that does.

Final Thoughts: Perspective for 2025 and Beyond

If you’re hoping for a return to 2.65% rates, history suggests that was the outlier, not the baseline. The average 30-year fixed rate since 2000 remains around 5.5%, and we are not far off from that now. The question for buyers and investors is not “When will rates drop?” but rather, “Is the current environment sustainable for my long-term goals?”

From an appraiser’s lens, the fundamentals still matter: location, condition, comparables, and credibility. Mortgage rates may rise and fall, but sound valuation principles are constant.

Need help interpreting market data for a property or preparing for an appraisal in this environment? Visit our blog archive for expert tips and tools designed for both professionals and homeowners.

Let data—not hype—guide your next real estate move.